This document is a commented summary of the Climate Impact Report released by the company ISS ESG[1] based on its proprietary methodology, concerning the holdings of Etica Sgr’s Fund Etica Impatto Clima (also referred to as “the portfolio”). The report includes metrics aligned with the guidelines of the Task Force on Climate-related Financial Disclosures (TCFD[2].).

All asset classes have been analysed according to the TCFD recommendations, grouped as follows: Equity Portfolio and Corporate Bonds Portfolio together and, Sovereign Bonds Portfolio.

The analysis outlines the climate performance calculated on the portfolio at the year-end of 2023 and compares it with the index MSCI World ESG Universal Net Total Return as a market benchmark (also referred to as “the benchmark”) on the same date. It is divided into the following sections: carbon metrics, scenario analysis, transitional climate risks analysis, physical risks, additional insights, and conclusions.

- Carbon metrics

- Comparison with Etica Impatto Clima year-end 2022

- Scenario Analysis

- Transitional climate risks analysis

- Physical risks

- Conclusions

- Sovereign bonds

Carbon metrics

The carbon metrics used in the Equity and Corporate Bonds analysis are the following ones and are explicitly recommended by the TCFD:

- Relative Carbon Footprint: defined as the total scope 1 and scope 2 GHG emissions of the portfolio, directly attributable to the investor through its ownership share in companies’ total market value (also defined as “Emissions Exposure”), per million EUR invested. It is measured in tCO2e/EUR million invested.

- Carbon intensity: defined as the total scope 1 and 2 GHG emission intensity of the portfolio (based on issuers’ revenues), directly attributable to the investor through its ownership share in the companies’ total market value. It is measured in tCO2e/EUR million revenue.

- The Weighted Average Carbon Intensity (WACI): expresses scope 1 and 2 GHG emission intensity (based on issuers’ revenues), proportional to the issuers’ weight in the portfolio. Hence, this does not take the ownership share into account. It is measured in tCO2e/EUR million revenue.

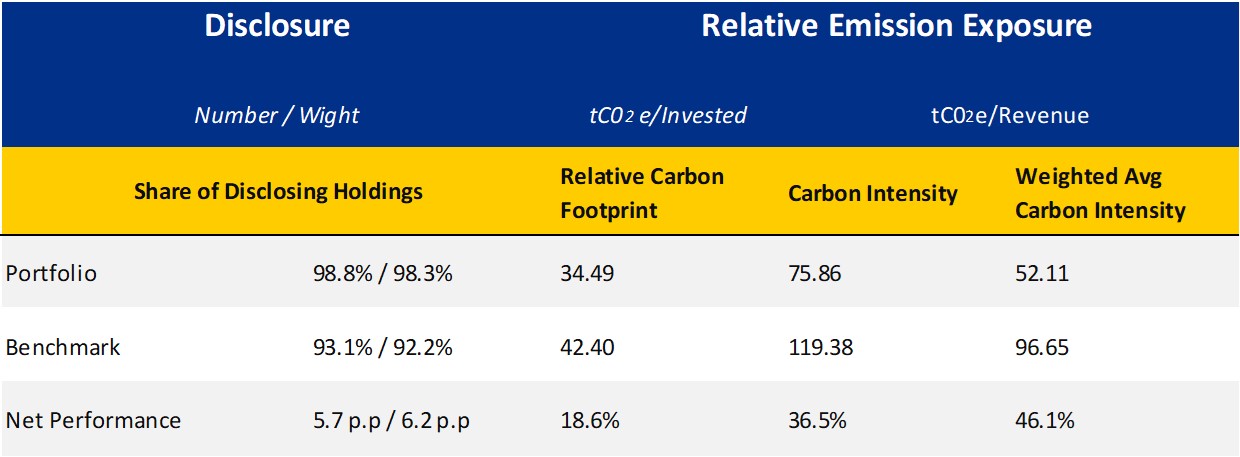

Overall, the relative carbon footprint of the portfolio amounts to 34,49 tCO2e/EUR million, which appears to be 18.6% lower than in the benchmark. The carbon intensity is 75,86 tCO2e/EUR million, 36,5% lower than the benchmark. The weighted average carbon intensity 52,11 tCO2e/EUR million, 46,1% lower than the benchmark. Note that 98.8% of the entities included in the portfolio disclose their scope 1 and scope 2 GHG emissions, compared to 93% in the benchmark.

This is a good improvement on last year’s analysis, when the fund didn’t outperform its benchmark. The main reason is the change in portfolio composition due to Etica Sgr’s selection methodology.

Comparison with Etica Impatto Clima year-end 2022

In December 2021, Etica adopted a stricter selection policy for companies involved in fossil fuels activities, including natural gas. In September 2022, the selection policy was further developed to include a specific climate impact assessment of companies involved in any fossil-related activities and those operating in Utilities, Materials and Industrial sectors with high emission intensity. In 2023, the climate assessment was applied to all the companies included in the Etica Impatto Clima funds.

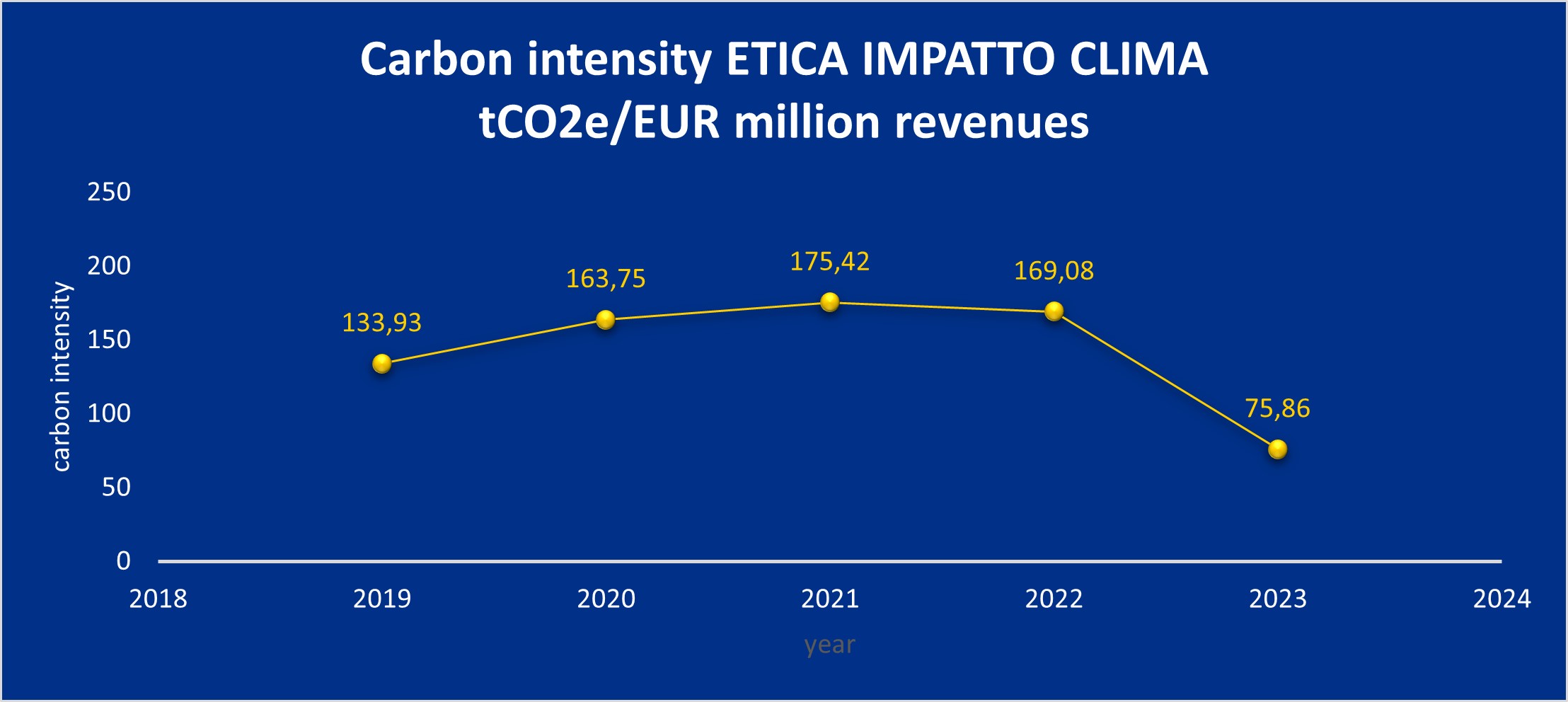

The change in carbon metrics over time for the portfolio is shown below.

| Year of reference | Relative carbon footprint tCO2e/EUR million invested | Carbon intensity

tCO2e/EUR million revenues |

WACI

tCO2e/EUR million revenuesi |

Carbon intensity Year on Year change (%) |

| 2019 | 78,31 | 133,93 | 92,13 | |

| 2020 | 107,97 | 163,75 | 164,54 | +22,27% |

| 2021 | 70,33 | 175,42 | 1054,56 | -+7,13% |

| 2022 | 74,33 | 169,08 | 148,04 | -3,61% |

| 2023 | 34,49 | 75,86 | 52,11 | -55,13% |

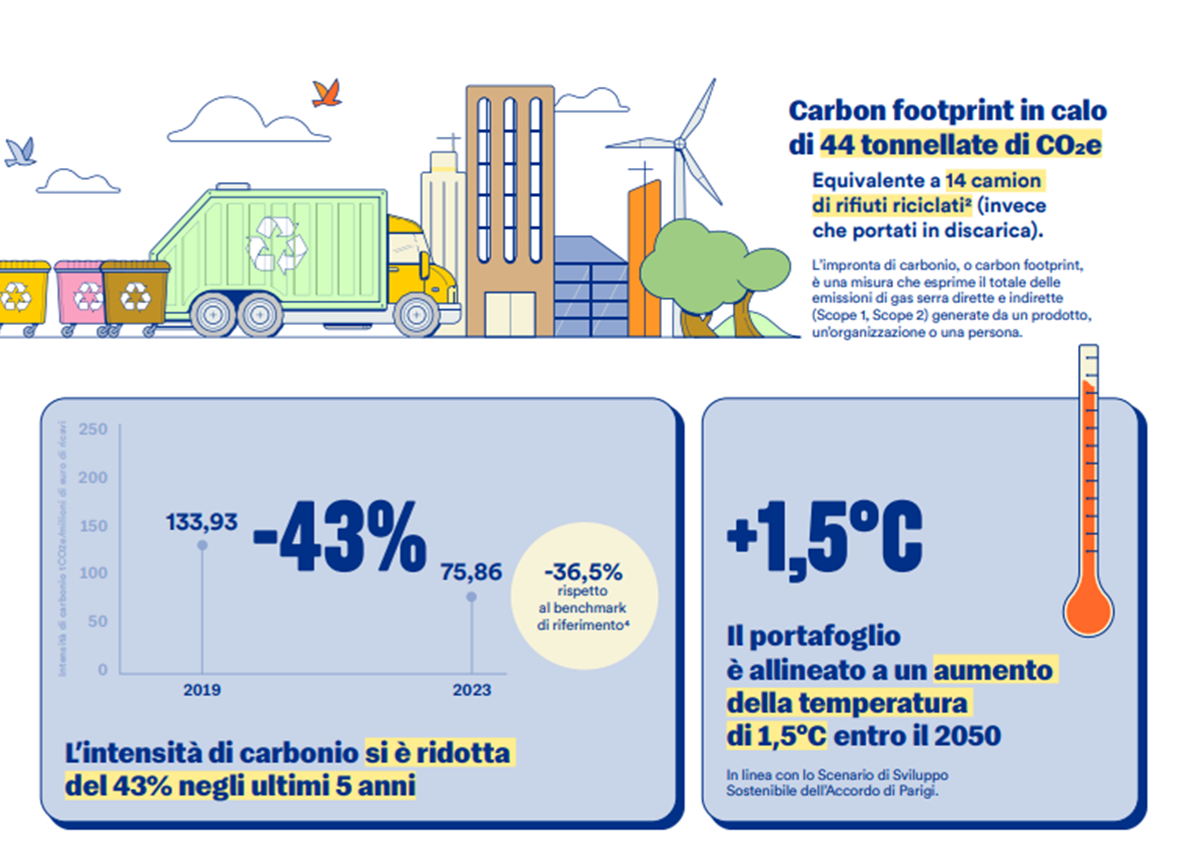

From 2021 to 2023 Etica Impatto Clima’s carbon intensity dropped by 55% and the scenario analysis confirms the portfolio is aligned with a Sustainable Development Scenario, as it is associated with a temperature increase of 1.5°C

In general, the yearly change in carbon intensity is driven by both changes in portfolio composition (especially as a consequence of specific interventions in the selection methodology) and a reduction in the emission intensity of companies.

It is possible to compare the portfolio at the end of 2023 with that at the end of 2022, using the latest available data in 2023 for both portfolios to isolate the specific effect of selection changes that affected the portfolio’s composition.

The carbon intensity of the portfolio at year-end 2022 was 169,08 tCO2e/EUR and that of the same portfolio with the latest available data at the end of 2023 is 136,79 tCO2e/MEur. Therefore, it can be calculated that:

| Carbon intensity change 2022-2023,

of wich |

55,13% |

| Difference in carbon intensity port 2022 – port 2022 (based on 2023 data) | 23,61% |

| Portfolio turnover effect on 2023-2022 change | 31,53% |

| This means that the 55.13% change in carbon intensity, normalizing all to 100, is due to: | |

| Change in portfolio composition, due to Etica methodology | 57,2% |

| Change in the emission data of issuers | 42,82% |

The change in carbon intensity from 2022 to 2023 is mainly due to changes in the companies in the portfolio, while improvements in company emissions have a minor but consistent weight in the improvement in carbon intensity.

Scenario Analysis

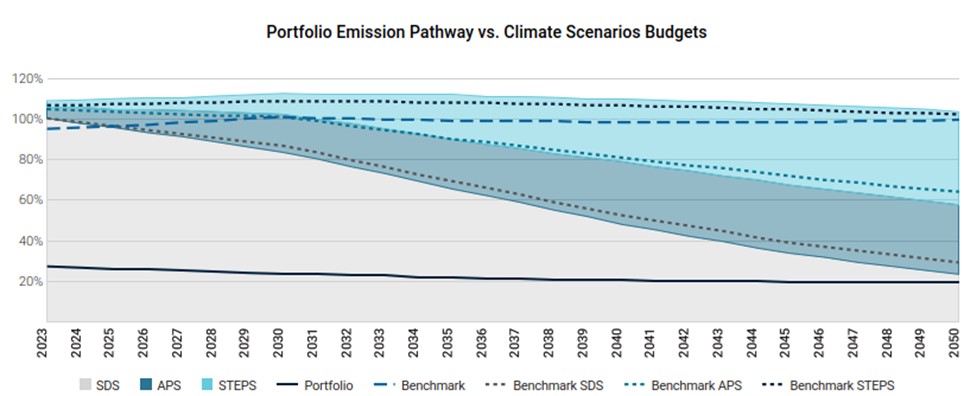

The purpose of the scenario analysis is to examine the current and future emission intensity from the direct and indirect emissions of a company (GHG scope 1&2) to see which climate scenario it is aligned with, until 2050. Each company’s carbon budget is defined based on its current and estimated future market share.

The scenario analysis compares current and future portfolio’s GHG emissions with the carbon budget estimated in different IEA scenarios: Sustainable Development Scenario (SDS)[3], Announced Pledges Scenario (APS) and Stated Policies Scenario (STEPS)[4]. Each scenario is tied to a carbon budget, i.e. a limited amount of fossil carbon that can be combusted worldwide to remain within a certain temperature. The carbon budget changes depending on the scenario, with the Sustainable Development Scenario being the most ambitious one, consistent with a global temperature increase well below 2°C by 2100, compared to pre-industrial levels. Performance is shown as a percentage of the allocated budget used by the portfolio and the benchmark.

The analysis shows that the current state of the portfolio is in line with a 2050 SDS scenario. This means that, for the first time, the Etica Impatto Clima Funds have a potential temperature increase of 1.5°C.

Conversely, the benchmark exceeds the budget of the SDS scenario in 2026 and is associated with a temperature increase of 2.7°C by 2050.

The better performance of the portfolio compared to the benchmark is explained by two factors, linked to the sectorial allocation and the single stock selection:

- The exclusion of most fossil activities from the portfolio;

- A higher number of companies with a commitment to reduce emissions.

Notably, 65% of the portfolio’s value (58% in the TCFD Report 2023) is covered by a GHG reduction target approved by the Science-Based Targets initiative (SBTi), against 48% of the market index.

Transitional climate risks analysis

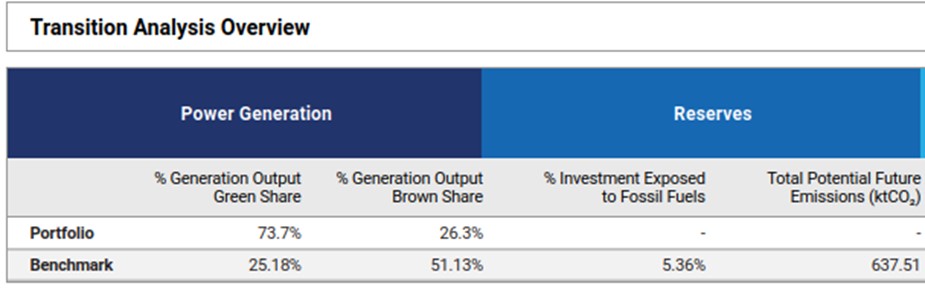

The analysis of transitional climate risks looks at the portfolio’s electricity generation mix.

Of the overall power generation installed capacity by companies in the portfolio, over 73,7% comes from renewables, against almost 26,3% from thermal power. This is a significant improvement on last year’s figure of 56.5%. In addition, the portfolio also outperformed the benchmark, with the share of renewable energy capacity at around 25% and the share of thermal capacity at almost 51%. Nuclear capacity is 26% in the benchmark and 0% in Etica Impatto Clima. There is no exposure to fossil fuel reserves.

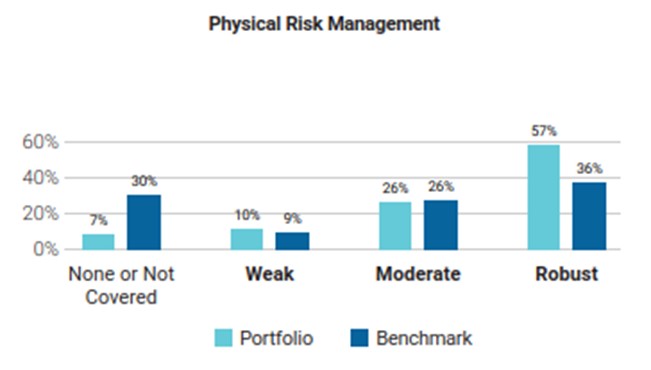

Physical risks

ISS employs a model to estimate the potential value losses, estimated by 2050, arising from the change in share price due to climate physical risks, computing the Value at Risk (VaR) of each issuer. The valuation model considers the following risks: changes in capital value via changes in Property, Plant and Equipment (PP&E), repair costs to damaged assets via investments in Capital Expenditure (CAPEX), increases in production costs via changes in Selling, General and Administrative Expenses, (SG&A) or Cost of Goods Sold (COGS), change in income via sales.

The analysis is based on the most relevant scenarios used as part of the IPCC 5th Assessment Report (AR5). The baseline scenario is built around Representative Concentration Pathway (RCP) 4.5 (1.7-3.2 ℃ temperature rise by 2100). In this scenario, the portfolio value at risk by 2050 is estimated to be 5.9 EUR million, with the Consumer Discretionary, Consumer Staples and Information technology being the most exposed ones. This represents a 0,5% loss in the overall fund value. The value at risk rises to over 9,26 EUR million if a worst-case scenario is employed, assuming a temperature increase over 3.2°C.

However, based on the ISS assessment, only the 10% of issuers have a weak physical risk management strategy and the 57% have a robust strategy.

Note that only 7% of Etica SGR companies are not covered, compared to 30% of the benchmark.

Conclusions

The specific climate assessment included in the methodology in 2023 proved highly effective in reducing the carbon footprint of the portfolio, especially by the means of the exclusion of most polluting companies in Materials and Industrial sectors.

The carbon intensity at the end of 2023 was almost 55% lower than at the end of 2022 and 43,36% lower than the portfolio at the end of 2019.

The scenario analysis shows that the portfolio at the end of 2023 is associated with a potential temperature increase of 1.5°C by 2050, a good improvement in comparison with the temperature increase of 1.7°C resulting in the analysis performed at the end of 2022. This means that for the first time, the resulting associated with a Sustainable Development Scenario.

Methodological improvements have ensured that most polluting companies are not invested, constant monitoring of the portfolio’s composition and balance would allow for better management of emissions.

Sovereign bonds

This Sovereign analysis compares the carbon emissions and other carbon related characteristics of the underlying portfolio with the benchmark. The tables below include absolute and relative figures for portfolio carbon emissions as well as intensity measures for both production and government emissions. The latest available reporting year is 2021 for Annex 1 Countries (UNFCCC) and 2020 for non-Annex 1 Countries (CAIT).

- “Emission Exposure” section measures the carbon footprint of a sovereign portfolio. Scope 1 Emissions are in tCO₂e while Scope 2 and Scope 3 Emissions are only in CO2

- Relative carbon footprint is defined as the total carbon emissions of the portfolio per million invested.

- Carbon intensity is expressed as the weighted average carbon emissions per million of PPP adj GDP as a proxy of the carbon efficiency per unit of output.

To account for the different calculation possibilities as well as to offer various perspectives, ISS ESG provides data for the following two different sovereign emission categories:

- Production Emissions: Emission footprint of a country’s production with its imports according to the latest PCAF guidelines released in December 2022.

- Government Emissions: This approach takes into account that a government bond co-finances both direct emissions from the public sector and investments made by the government.

Production emissions

Governament Emissions

In general, the performance of the fund is in line with the benchmark. The better performance compared to the portfolio at the end of 2022 is due to the new composition of the portfolio, which is now more in line with the benchmark.

It is important to note that the selection methodology for the State on environmental prospective is the same between Impatto Clima and Valori Responsabili, so the difference between the performance of these two funds is due to the weighting of the issuer.

Climate Impact in Brief

References

[1] https://www.issgovernance.com/esg/

[2] Launched after the 2015 Paris Agreement by the Financial Stability Board (FSB), the Task Force on Climate-related Financial Disclosure (TCFD – https://www.fsb-tcfd.org/) considers climate transparency as a crucial factor for the stability of financial markets. The objective of the TCFD is therefore to improve climate transparency in financial markets through recommendations on disclosure. These recommendations provide a “consistent framework that improves the ease of both producing and using climate-related financial disclosures”. The TCFD aims to create a unique standard for both corporate and investment disclosure, understanding that local regulatory frameworks may require different compliance levels. By October 12, 2023, the TCFD had fulfilled its mission and disbanded, although it remains a valid guideline for assessing and reporting on climate-related risks.

[3] The Sustainable Development Scenario is not more developed in the World Energy Outlook 2022 by the International Energy Agency. However, to guarantee comparability with previous years, this edition of the report still relies on it.

[4] Details on the scenarios and on underlying assumptions are available at World Energy Model – Analysis – IEA

This is a marketing communication.

Marketing communication by Etica SGR S.p.A. Investors should only make an investment decision after fully understanding the overall characteristics and level of risk exposure involved, by carefully reading the KID and the Prospectus of the individual funds. These documents – along with information on sustainability aspects pursuant to Regulation (EU) 2019/2088 – are available on the website www.eticasgr.com. The recipients of this message bear full and sole responsibility for the use of the information contained in this communication, as well as for any investment decisions possibly made on the basis of it, since any use of this information as a support for investment decisions is not permitted and is entirely at the investor’s own risk.

– SICAV")

VALORI RESPONSABILI 2024")